By Lauren Van Buren

It is no surprise that Americans are willing to make sacrifices in exchange for convenience. The way we manage our finances is no exception. In a 2017 survey, 62 percent of smartphone owners stated that they used an online banking application, and 26 percent said they wanted their mobile devices to track their spending. Meanwhile, only 10 to 14 percent of Americans still use cash as their primary form of payment.

For those in the 26 percent, financial data aggregation platforms such as Mint and Personal Capital allow users to view their investments, savings, insurance policies, and credit balances in one spot, often referred to as a “dashboard” or “hub.” To effectuate this objective, customers agree to provide the application with the login credentials for all of their financial accounts.

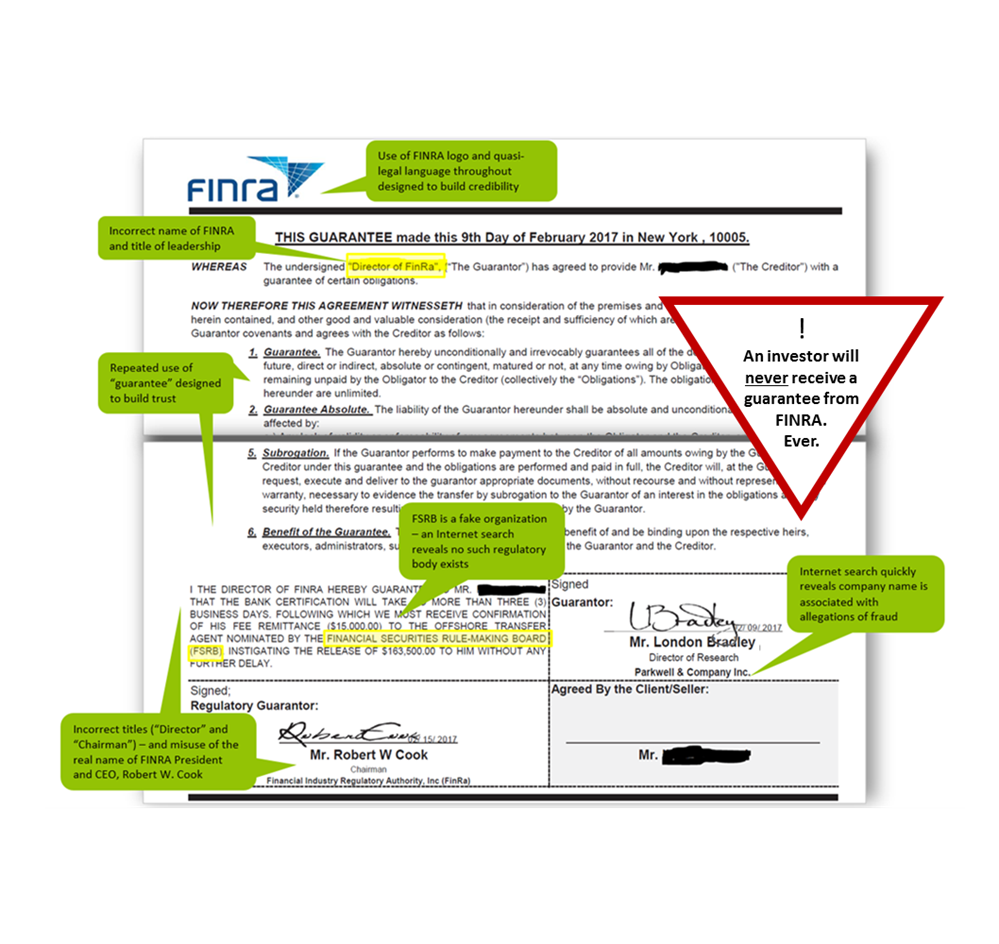

The Financial Industry Regulatory Authority (FINRA) recently issued an Investor Alert warning investors about the risks of using financial data aggregation platforms. Specifically, the Alert cautions consumers about the potential increased vulnerability to cyber fraud, unauthorized transactions, and identity theft. While these platforms are not presumptively unsafe, individuals should take precautions before handing over their login credentials.

Research the company providing the service. A quick Google search can help identify users that have experienced security issues with the platform. Moreover, ensure the company prioritizes security by offering two-factor authentication.

Create the account using a different email address. If your primary email account is hacked, the hacker might be able to reset your password on the data aggregation platform to gain access. To mitigate this risk, use a unique email address when you sign up for the financial aggregation service. An email address that you have not provided to other third parties is much less likely to be the target of a phishing attack.

Monitor your accounts to quickly detect identity theft. Each of the nationwide credit reporting companies are required to provide consumers with a free credit report once every 12 months upon request. Take advantage of this, regardless of whether you elect to use a financial data aggregation platform.

Read the terms and conditions. Read the user agreement to ensure you are not authorizing the application to use your financial data for any other purpose, or make payments on your behalf. Moreover, you should verify that the platform will access only the information it needs to provide the service to you.

One article suggests that data aggregation technology should be used in evaluating an individual’s creditworthiness. This process would enable a bank to review an applicant’s recent transaction history to assess the applicant’s ability to repay a loan. If this makes you uncomfortable, you should avoid signing up for a platform that collects all of your account information and retains the right to share this information with third parties.

{kind=link}